Press Releases

Want to know what's new with us? Here's where you'll find the latest news about events, services and much more.

C&N Declares Dividend and Announces Third Quarter 2021 Unaudited Financial Results

Wellsboro, PA – Citizens & Northern Corporation (“C&N”) (NASDAQ: CZNC) announced its most recent dividend declaration and its unaudited, consolidated financial results for the three-month and nine-month periods ended September 30, 2021.

Dividend Declared

On October 21, 2021, C&N’s Board of Directors declared a regular quarterly cash dividend of $0.28 per share. The dividend is payable on November 12, 2021 to shareholders of record as of November 1, 2021.

Unaudited Financial Information

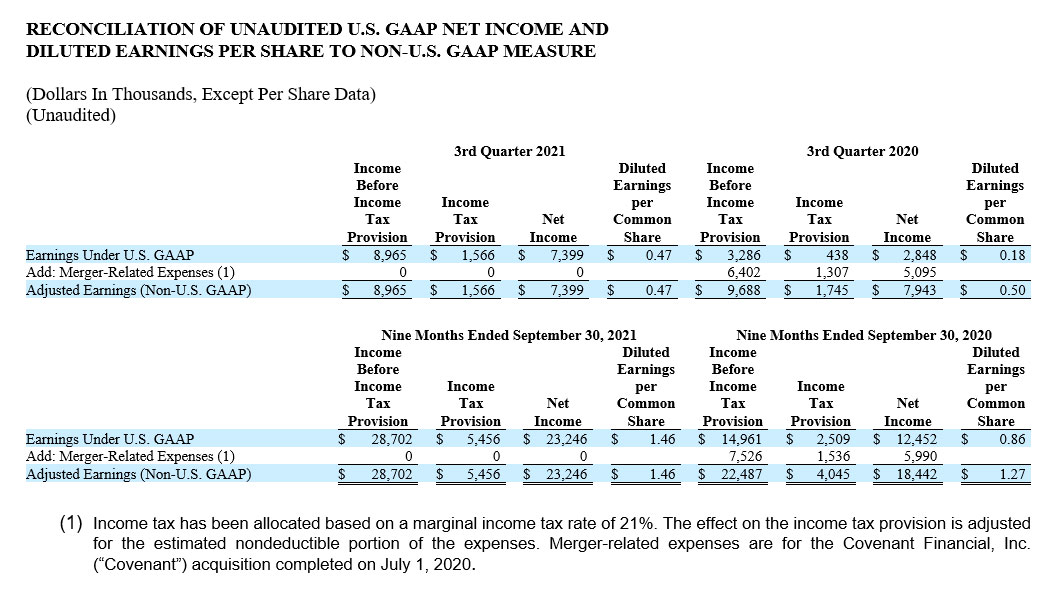

Net income was $0.47 per diluted share in the third quarter 2021, up from $0.44 in the second quarter 2021 and up $0.29 from $0.18 in the third quarter 2020. For the nine months ended September 30, 2021, net income per diluted share was $1.46, up from $0.86 per share for the first nine months of 2020. As described below, earnings of $0.47 per share for the third quarter 2021 were 6.0% lower than third quarter 2020 non-U.S. generally accepted accounting principles (U.S. GAAP) earnings per share of $0.50 as adjusted to exclude the impact of merger-related expenses. For the nine months ended September 30, 2021, earnings of $1.46 per share were 15.0% higher than the first nine months of 2020 non-U.S. GAAP earnings per share of $1.27 as adjusted to exclude the impact of merger-related expenses.

The following table provides a reconciliation of C&N’s unaudited earnings results under U.S. GAAP to comparative non-U.S. GAAP results excluding merger-related expenses. Management believes disclosure of unaudited earnings results for the periods presented, adjusted to exclude the impact of these items, provides useful information to investors for comparative purposes.

Highlights related to C&N’s third quarter and September 30, 2021 year-to-date unaudited U.S. GAAP earnings results as compared to the second quarter 2021 and the third quarter of 2020 are presented below.

Third Quarter 2021 as Compared to Second Quarter 2021

Net income was $7,399,000, or $0.47 per diluted share, for the third quarter 2021 as compared to $7,060,000, or $0.44 per diluted share, in the second quarter 2021.

- Net interest income totaled $19,459,000 in the third quarter 2021, up $778,000 from the second quarter 2021 amount of $18,681,000. The net interest rate spread increased 0.09%, as the average yield on earning assets increased 0.04% to 3.89% while the average rate on interest-bearing liabilities decreased 0.05% to 0.43%. The net interest margin was 3.59% in the third quarter 2021, up from 3.52% in the second quarter. Total interest and fees from loans originated under the U.S. Small Business Administration (SBA) Paycheck Protection Program (PPP) were $1,639,000 in the third quarter 2021, an increase of $390,000 from the second quarter 2021 total. The increase in income from PPP loans resulted from an increase in volume of loans processed for the SBA’s repayment tied to the forgiveness of the underlying borrowers. Accretion and amortization of purchase accounting adjustments had a net positive impact on net interest income of $563,000 in the third quarter 2021 as compared to a net positive impact of $713,000 in the second quarter 2021.

- The provision for loan losses was $1,530,000 in the third quarter 2021, an increase in expense of $786,000 from the second quarter 2021 provision of $744,000. The third quarter provision included a net charge of $611,000 related to specific loans (net charge-offs of $1,205,000 offset by a net decrease in specific allowances on loans of $594,000), and an increase of $919,000 in the collectively determined portion of the allowance. In the third quarter 2021, C&N recorded a partial charge-off of $1,194,000 on a commercial loan with an outstanding balance of $3,496,000 at the time of the charge-off. The partial charge-off amount exceeded the specific allowance of $583,000 that had been established at June 30, 2021.

- Noninterest income was $6,359,000 in the third quarter 2021, up $59,000 from the second quarter 2021 amount. Significant variances included the following:

- Service charges on deposit accounts of $1,249,000 in the third quarter 2021 were up $176,000 from the second quarter amount, as the volume of overdraft and other activity increased.

- Brokerage and insurance revenue of $560,000 increased $54,000 from the second quarter 2021 total, due to commissions on higher transaction volume.

- Net gains from sales of loans totaled $797,000 in the third quarter 2021, a decrease of $129,000 from the second quarter 2021 total, reflecting a reduction in volume of residential mortgage loans sold.

- Noninterest expense of $15,346,000 decreased $53,000 in the third quarter 2021 from the second quarter 2021 amount. Significant variances included the following:

- Salaries and employee benefits of $9,427,000 decreased $72,000 from the second quarter 2021 total, including a reduction in severance and estimated incentive compensation expense, partially offset by increases in lending, human resources and information technology personnel.

- Professional fees of $538,000 decreased $60,000 from the second quarter 2021 total, including a reduction in recruiting services and PPP loan processing professional fees.

- Other noninterest expense of $1,850,000 increased $99,000 from the second quarter 2021 total. Within this category, the allowance for SBA claim adjustments decreased $45,000 in the third quarter 2021, resulting in a reduction in expense, as compared to a reduction in expense of $163,000 from a reduction in the allowance in the second quarter 2021.

- The income tax provision was $1,566,000 for the third quarter 2021, down from $1,780,000 for the second quarter 2021. In the third quarter 2021, the provision for state and local income taxes was reduced based on adjustments to apportionment estimates and other factors.

Third Quarter 2021 as Compared to Third Quarter 2020

As described above, third quarter 2021 net income was $7,399,000. In comparison, third quarter 2020 net income was $2,848,000, and excluding merger-related expenses, adjusted (non-U.S. GAAP) earnings were $7,943,000. Other significant variances were as follows:

- Third quarter 2021 net interest income of $19,459,000 was $177,000 higher than the third quarter 2020 total. Average outstanding loans decreased $113.7 million, including a reduction in average PPP loans of $74.5 million, and average total deposits increased $52.2 million. The net interest margin for the third quarter 2021 was 3.59% as compared to 3.57% for the third quarter 2020. The average yield on earning assets of 3.89% for the third quarter 2021 was down 0.13% from the third quarter 2020, while the average rate on interest-bearing liabilities of 0.43% in the third quarter 2021 was 0.19% lower than the comparable third quarter 2020 average rate. Interest and fees on PPP loans totaled $1,639,000 in the third quarter 2021, an increase of $750,000 over the third quarter 2020 amount. Accretion and amortization of purchase accounting adjustments had a net positive impact on net interest income of $563,000 in the third quarter 2021 as compared to a net positive impact of $1,298,000 in the third quarter 2020.

- The provision for loan losses was $1,530,000 in the third quarter 2021 as compared to $1,941,000 in the third quarter 2020. Details concerning the third quarter 2021 provision for loan losses were described previously. The provision for loan losses in the third quarter 2020 included the net impact of a charge-off of $2,219,000 on a commercial loan of $3,500,000 for which the previously-established allowance had been $1,193,000.

- Noninterest income for the third quarter 2021 was down $611,000 from the third quarter 2020 total. Significant variances included the following:

- Net gains from sales of loans of $797,000 for the third quarter 2021 were down $1,255,000 from the total for the third quarter 2020, as the volume of residential mortgage loans sold in the third quarter 2021 was down from the third quarter 2020 level.

- Other noninterest income totaled $665,000, a decrease of $331,000 from the third quarter 2020 as C&N recognized income of $279,000 in the third quarter 2020 from a life insurance arrangement in which benefits were split between C&N and heirs of a former employee and dividend income from Federal Home Loan Bank stock decreased $55,000.

- Loan servicing fees, net, were $153,000 in the third quarter 2021, an increase of $240,000 over the third quarter 2020 reduction in revenue of $87,000. The net increase reflects growth in volume of residential mortgage loans sold with servicing retained. Further, the fair value of servicing rights decreased $45,000 in the third quarter 2021 as compared to a reduction in fair value of $221,000 in the third quarter 2020, as market assumptions regarding prepayment speeds have decreased.

- Trust revenue of $1,821,000 increased $226,000 reflecting the impact of growth in trust assets under management including the impact of market value appreciation.

- Service charges on deposit accounts of $1,249,000 in the third quarter 2021 were up $204,000 from the third quarter 2020 amount, as the volume of consumer and business overdraft and other activity increased.

- Brokerage and insurance revenue of $560,000 increased $178,000 from the third quarter 2020 total, due to commissions on higher transaction volume.

- Interchange revenue from debit card transactions totaled $975,000 in the third quarter 2021, an increase of $147,000 over the third quarter 2020 total, reflecting increases in transaction volumes and number of accounts due to the Covenant acquisition.

- Noninterest expense, excluding merger-related expenses, increased $698,000 in the third quarter 2021 over the third quarter 2020 amount. Significant variances included the following:

- Salaries and employee benefits of $9,427,000 increased $724,000, including the impact of increases in administrative, information technology, cash management services and lending personnel.

- Professional fees of $538,000 increased $116,000, including increases in recruiting services.

- Other noninterest expense of $1,850,000 decreased $240,000, including other operational losses decreasing $195,000 as an estimated accrual of $200,000 related to a Trust Department tax compliance and preparation matter was recorded in the third quarter 2020 with no comparable charge in the third quarter 2021.

- The income tax provision of $1,566,000 for the third quarter 2021 was up $1,128,000 from $438,000 for the third quarter 2020, reflecting higher pre-tax income.

Nine Months Ended September 30, 2021 as Compared to Nine Months Ended September 30, 2020

Net income for the nine-month period ended September 30, 2021 was $23,246,000, or $1.46 per diluted share, while net income for the first nine months of 2020 was $12,452,000, or $0.86 per share. Excluding the impact of merger-related expenses, adjusted (non-U.S. GAAP) earnings for the first nine months of 2020 would be $18,442,000 or $1.27 per share. Other significant variances were as follows:

- Net interest income was up $10,413,000 (21.8%) for the first nine months of 2021 over the same period in 2020, reflecting growth mainly attributable to the Covenant acquisition. Average outstanding loans increased $241.3 million, and average total deposits increased $396.7 million. The net interest margin was 3.70% for the nine months ended September 30, 2021, up from 3.67% for the first nine months of 2020. Interest and fees on PPP loans totaled $4,886,000 for the first nine months of 2021, an increase of $3,457,000 compared to the first nine months of 2020. Accretion and amortization of purchase accounting adjustments had a net positive impact on net interest income of $2,228,000 in the first nine months of 2021 as compared to a net positive impact of $1,999,000 in the first nine months of 2020.

- For the first nine months of 2021, the provision for loan losses was $2,533,000, a decrease in expense of $760,000 as compared to $3,293,000 recorded in the first nine months of 2020. The provision for the first nine months of 2021 includes the impact of a charge-off of $1,194,000 on a commercial loan with an outstanding balance of $3,496,000, as previously discussed. In comparison, the provision for loan losses in the first nine months of 2020 included the impact of the $2,219,000 charge-off of a commercial loan of $3,500,000.

- Noninterest income for the first nine months of 2021 was up $1,662,000 from the total for the first nine months of 2020. Significant variances included the following:

- Loan servicing fees, net, were $547,000 in the first nine months of 2021, an increase of $806,000 over the 2020 total of negative $259,000 (a decrease in revenue). The net increase reflects growth in volume of residential mortgage loans sold with servicing retained. Further, the fair value of servicing rights decreased $9,000 in the first nine months of 2021 as compared to a reduction in fair value of $617,000 in 2020 mainly due to changes in assumptions related to prepayments of mortgage loans.

- Trust revenue of $5,254,000 increased $615,000 reflecting the impact of growth in average trust assets under management including the impact of market value appreciation.

- Interchange revenue from debit card transactions totaled $2,786,000 for the first nine months of 2021, an increase of $577,000, reflecting an increase in transaction volumes.

- Brokerage and insurance revenue of $1,392,000 increased $271,000, due to commissions on higher transaction volume.

- Other noninterest income totaled $2,837,000, an increase of $254,000 over 2020. Within this category, significant variances included the following:

- Income from realization of tax credits was $268,000 higher in the first nine months of 2021 as compared to 2020 due to higher PA Educational Improvement Tax Credit Program donations.

- Fee income for providing credit enhancement on sale of mortgage loans increased $158,000.

- Credit card interchange income increased $69,000 due to higher transaction volume.

- Income from investment in a title agency increased $54,000.

- Merchant services income increased $43,000.

- Other noninterest income decreased $279,000 due to the impact of the life insurance transaction in 2020 described above.

- Dividend income from Federal Home Loan Bank stock decreased $76,000.

- Service charges on deposit accounts of $3,337,000 in the first nine months of 2021 increased $211,000 from the total for the first nine months of 2020, as consumer and business activity increased.

- Net gains from sales of loans totaled $2,786,000 in the first nine months of 2021, a decrease of $1,145,000 from the total for the first nine months of 2020. The decrease reflects a decrease in volume of mortgage loans sold, resulting mainly from lower refinancing activity and overall market conditions.

- Noninterest expense, excluding merger-related expenses, increased $6,620,000 for the nine months ended September 30, 2021 over the total for the first nine months of 2020. Significant variances included the following:

- Total salaries and wages and benefits expenses increased $4,757,000, reflecting inclusion of the former Covenant operations for nine months in 2021 as compared to three months in 2020, as well as increases in lending, human resources, information technology and other personnel needed to accommodate growth.

- Net occupancy and equipment expense increased $473,000, primarily reflecting an increase due to the Covenant acquisition.

- Data processing and telecommunications expenses increased $383,000, including the impact of growth related to the Covenant acquisition, increased costs from outsourced support services and other increases in software licensing and maintenance costs.

- Professional fees expense increased $302,000, mainly due to increases in recruiting services and PPP loan processing professional fees.

- Other noninterest expense increased $256,000. Within this category, significant variances included the following:

- FDIC insurance expense totaled $431,000, an increase of $244,000.

- Donations expense increased $230,000, mainly due to an increase in donations associated with the PA Educational Improvement Tax Credit program.

- Business development expenses totaled $345,000, an increase of $201,000, due primarily to an increase in public relations expense.

- Other operational losses totaled $159,000, a decrease of $394,000, including a reduction in charges related to Trust Department tax compliance and preparation matters.

- The allowance for SBA claim adjustments decreased, reflecting more favorable claim results than previously estimated, resulting in a reduction in expense of $208,000.

- The income tax provision was $5,456,000 for the nine months ended September 30, 2021, up from $2,509,000 for the first nine months of 2020. Pre-tax income was $13,741,000 higher in the first nine months of 2021 as compared to 2020. The effective tax rate was 19.0% for the first nine months of 2021, higher than the 16.8% effective tax rate for the first nine months of 2020. The tax benefit of tax-exempt interest income was 2.4% of pre-tax income in the first nine months of 2021 as compared to a 5.0% benefit in 2020.

Other Information:

Changes in other unaudited financial information are as follows:

- Total assets amounted to $2,354,896,000 at September 30, 2021, up from $2,339,063,000 at June 30, 2021 and up slightly from $2,352,793,000 at September 30, 2020.

- Net loans outstanding (excluding mortgage loans held for sale) were $1,563,008,000 at September 30, 2021, down from $1,585,481,000 at June 30, 2021 and down 7.0% from $1,680,617,000 at September 30, 2020. Loans outstanding, excluding PPP loans, totaled $1,512,980,000 at September 30, 2021, an increase of $25,435,000 from total loans excluding PPP at June 30, 2021. In comparing outstanding balances at September 30, 2021 and 2020, total commercial loans were down $55.8 million (5.4%), including a reduction in PPP loans of $100.3 million and an increase in other commercial loans of $44.5 million, total residential mortgage loans were lower by $60.2 million (9.4%) and total consumer loans were up $0.3 million (1.5%). The outstanding balance of residential mortgage loans originated and serviced by C&N that have been sold to third parties was $328.7 million at September 30, 2021, up $74.2 million (29.2%) from September 30, 2020.

- To work with clients impacted by COVID-19, C&N offers short-term loan modifications (deferrals) on a case-by-case basis to borrowers who were current in their payments prior to modification. These loans are not reported as past due or troubled debt restructurings during the deferral period. At September 30, 2021, there were no loans in deferral status under the program. In comparison, at June 30, 2021, C&N had 12 loans with an aggregate recorded investment of $6.7 million in deferral status and at September 30, 2020, there were 44 loans with an aggregate recorded investment of $44.6 million in deferral status.

- Total nonperforming assets as a percentage of total assets was 1.05% at September 30, 2021, as compared to 1.12% at June 30, 2021 and down from 1.17% at September 30, 2020. Total nonperforming assets were $24.6 million at September 30, 2021, down from $26.2 million at June 30, 2021 and $27.5 million at September 30, 2020.

- The allowance for loan losses was $12.7 million at September 30, 2021, or 0.81% of total loans as compared to $12.4 million or 0.77% of total loans at June 30, 2021. In 2020 and 2019, C&N recorded performing loans purchased from other financial institutions at fair value. The calculations of fair value included discounts for credit losses, reflecting an estimate of the present value of credit losses based on market expectations. The total allowance for loan losses and the credit adjustment on purchased non-impaired loans at September 30, 2021 was $16.5 million, or 1.05% of total loans receivable and the credit adjustment. The comparative ratios were 1.05% at June 30, 2021 and September 30, 2020.

- Deposits totaled $1,940,141,000 at September 30, 2021, up from $1,916,809,000 at June 30, 2021, and up 3.7% from $1,871,514,000 at September 30, 2020.

- Total stockholders’ equity was $299,402,000 at September 30, 2021, down from $304,133,000 at June 30, 2021 and up from $296,316,000 at September 30, 2020. Within stockholders’ equity, the portion of accumulated other comprehensive income related to available-for-sale debt securities was $6,300,000 at September 30, 2021, down from $9,167,000 at June 30, 2021 and $11,376,000 at September 30, 2020. Fluctuations in accumulated other comprehensive income related to valuations of available-for-sale debt securities have been caused by changes in interest rates

- In February 2021, C&N amended its existing treasury stock repurchase program. Under the amended program, C&N is authorized to repurchase up to 1,000,000 shares of the Corporation’s common stock, or 6.25% of the Corporation’s issued and outstanding shares at February 18, 2021. In the third quarter 2021, 230,404 shares were repurchased for a total cost of $5,707,000, at an average price of $24.77 per share. Cumulatively through September 30, 2021, 292,100 shares have been repurchased for a total cost of $7,238,000, at an average price of $24.78 per share.

- In May 2021, C&N completed a private placement of $25 million of 3.25% Fixed-to-Floating Rate Subordinated Debt due 2031 and $15 million of 2.75% Fixed Rate Senior Unsecured Notes due 2026. The Subordinated Debt is intended to qualify as Tier 2 capital. In June 2021, a portion of the proceeds was used to redeem subordinated debt with par values totaling $8 million. The remaining proceeds are available for general corporate purposes.

- Citizens & Northern Bank is subject to various regulatory capital requirements. At September 30, 2021, Citizens & Northern Bank maintains regulatory capital ratios that exceed all capital adequacy requirements. Management expects the Bank to remain well-capitalized for the foreseeable future.

- Trust assets under management by C&N’s Wealth Management Group amounted to $1,183,900,000 at September 30, 2021, down 0.8% from $1,192,928,000 at June 30, 2021 and up 16.9% from $1,012,986,000 at September 30, 2020. Fluctuations in values of assets under management reflect the impact of high recent market volatility.

Citizens & Northern Corporation is the bank holding company for Citizens & Northern Bank, headquartered in Wellsboro, Pennsylvania which operates 30 banking offices located in Bradford, Bucks, Cameron, Chester, Lycoming, McKean, Potter, Sullivan Tioga and York Counties in Pennsylvania and Steuben County in New York, as well as a loan production office in Elmira, New York. Citizens & Northern Corporation trades on NASDAQ under the symbol “CZNC.” For more information about Citizens & Northern Bank and Citizens & Northern Corporation, visit www.cnbankpa.com.

Safe Harbor Statement: Except for historical information contained herein, the matters discussed in this release are forward-looking statements. Investors are cautioned that all forward-looking statements involve risks and uncertainty, including without limitation, the following: the effect of COVID-19 and related events, which could have a negative effect on C&N’s business prospects, financial condition and results of operations, including as a result of quarantines; market volatility; market downturns; changes in consumer behavior; business closures; deterioration in the credit quality of borrowers or the inability of borrowers to satisfy their obligations to C&N (and any related forbearances or restructurings that may be implemented); changes in the value of collateral securing outstanding loans; changes in the value of the investment securities portfolio; effects on key employees, including operational management personnel and those charged with preparing, monitoring and evaluating the companies’ financial reporting and internal controls; declines in the demand for loans and other banking services and products, as well as increases in non-performing loans, owing to the effects of COVID-19 in the markets served by C&N and in the United States as a whole; declines in demand resulting from adverse impacts of the disease on businesses deemed to be “non-essential” by governments and individual customers in the markets served by C&N; or branch or office closures and business interruptions triggered by the disease; changes in monetary and fiscal policies of the Federal Reserve Board and the U.S. Government, particularly related to changes in interest rates; changes in general economic conditions caused by factors other than COVID-19; legislative or regulatory changes; downturn in demand for loan, deposit and other financial services in the Corporation’s market area; increased competition from other banks and non-bank providers of financial services; technological changes and increased technology-related costs; changes in management’s assessment of realization of securities and other assets; and changes in accounting principles, or the application of generally accepted accounting principles. Citizens & Northern disclaims any intention or obligation to publicly update or revise any forward-looking statements, whether as a result of events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.